European secondary equity market structure has emerged as a central focus in negotiations around the EU’s Market Integration and Supervision Package (MISP) – a landmark set of reforms designed to improve the competitiveness of EU capital markets. Alongside this, ESMA’s recent ‘call for evidence’ on European equity market structure offered a timely opportunity to assess the current framework and inform how best to move it forward under MISP.

Cboe Europe welcomed the opportunity to contribute to this process, bringing our unique perspective as the region’s largest equities exchange by value traded, and a deep commitment to a competitive, investor-focused and pan-European market structure.

Our core message is simple: the secondary market is performing well amid record levels of investor interest, and the competitive framework built under Mifid I and Mifid II is delivering. MISP should

build on – not disrupt – this positive momentum. Whilst there is room to strengthen EU capital markets, particularly when it comes to the IPO and post-trade ecosystems, wholesale reform of secondary markets isn’t necessary. Instead, targeted refinements would be most effective.

ESMA paints positive picture of European markets

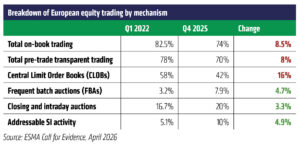

The ‘call for evidence’ was underpinned by ESMA’s detailed analysis of transaction reporting data from Q1 2022 to Q4 2025 (see table).

The key takeaway is one of strength: on-book trading is high and stable, with pre-trade transparent venues – and Central Limit Order Books (CLOBs) in particular – the main sources of liquidity and strong centres of price formation. This is not a market in crisis, and stands in sharp contrast to the exaggerated – albeit persistent – claims from certain vested interests that dark and off-book mechanisms have grown excessively at the expense of lit markets. What we are seeing is a redistribution of activity across a broader range of venues and mechanisms that, in most cases, deliver materially better outcomes for investors.

Competition and diversity of trading mechanisms is working – Don’t reverse it

ESMA’s analysis – reinforced by recent periods of elevated market activity – shows that competition in equity trading is working well, and investors have never had it better in terms of execution quality, trading costs, and choice of venue. The growth of alternative mechanisms reflects evolving investor needs and increasingly sophisticated execution strategies, not any fundamental weakness in European market structure.

A well-functioning European equity market requires a range of mechanisms that serve the different needs participants. CLOBs provide continuous liquidity and price discovery for urgent order flow. Closing auctions aggregate end-of-day demand at a single reference price. Frequent Batch Auctions (FBAs) provide a transparent, on-venue mechanism for investors to find counterparties without being disadvantaged by latency. SIs offer differentiated liquidity via capital commitment. Each has a role; none is a substitute for the others.

Any measures restricting the way institutional equity trading business can execute within the EU will likely drive flow away from the region, undermining the EU’s regulatory objectives and overall competitiveness.

Innovation, not regulatory intervention, is key to growing CLOBs

Cboe Europe is a strong advocate for CLOBs – we operate one of the largest in the EU and are always innovating to grow this segment of the market. Yet experience has consistently shown that artificially promoting CLOBs through restrictions on other venues tend to backfire, often diverting flow to more opaque mechanisms. Responsibility for strengthening lit markets should rest with exchanges themselves, supported by a framework that promotes competition, innovation, and investor choice.

One of the most promising avenues for strengthening CLOBs is through greater incorporation of retail order flow. We are doing our part through the recent launch of our own pan-European retail service, offering brokers free of execution of retail orders at or better than the EBBO, helping to channel more retail onto our lit venues. We believe the EU should consider whether retail orders ought to be encouraged to execute on multilateral venues, improving markets for all participants.

Frequent batch auctions: A European success story

The growth of FBAs to represent a meaningful share of European equity trading is one of Europe’s great market structure success stories. As pioneer of the model in Europe, our service was developed in direct response to client demand for a low-impact execution mechanism that removes the structural advantages of speed while at the same time contributing to price formation and pre-trade transparent lit markets. FBAs batch orders over a short, randomised call period before matching them at a single clearing price, with full pre-trade transparency via a displayed indicative price and volume throughout.

A persistent misconception is that periodic auctions are a form of dark trading. This is incorrect. PABs are fully lit, on-venue mechanisms operating under the Mifir pre-trade transparency framework – following the transparency model of closing auctions, which are universally accepted as an important part of market structure. Furthermore, a key argument sometimes advanced against PABs is that they are price-referencing rather than price-forming. Real world data robustly contradicts this. Assessed against measurable indicators – including multilateral participation rates, broker preferencing levels, off-midpoint order incidence, and price distribution relative to prevailing spreads – Cboe’s FBA is unambiguously price-forming.

A level playing field for midpoint executions

We welcomed ESMA’s decision to withdraw its Q&A on the application of the tick size regime to FBAs when announcing its Call for Evidence back in April. Midpoint pricing – including where it falls on a half tick – is a widely recognised, valid, and fair price point, and it should be available across all trading mechanisms. When neither buyer nor seller has an urgent need for liquidity, the true midpoint is the fairest price.

Mifir reforms in March 2024 explicitly permitted SI midpoint executions off-tick, and the impact was immediate: off-tick midpoint trades rose from approximately 10% to around 60% of all SI midpoint trades in French and Dutch equities following the rule relaxation, according to Cboe analysis. To maintain genuine parity between SIs and multilateral venues, midpoint half-tick executions must be clearly codified and permitted for all on-venue mechanisms.

Conclusion

ESMA’s own data confirms it: European equity markets are in good health. The task now is to build on what is working – a competitive, diverse ecosystem that serves investors, advances the EU’s Savings and Investment Union agenda, and supports the long-term competitiveness of European capital markets.